Dashdot was an Australian property investment advisory and buyers’ agency that helped clients purchase investment properties using a data‑driven, portfolio‑building model. It operated nationally and positioned itself as a “high‑tech, high‑touch” partner for long‑term property investors.

However, Dashdot collapsed and entered voluntary liquidation on 28 May 2026 after a combination of severe financial pressures:

- Negative gearing and CGT tax changes that hit investor demand

- Weak consumer confidence

- Tighter lending conditions

- A surge in Meta (Facebook/Instagram) advertising costs, which doubled customer‑acquisition costs and halved revenue

- A business model heavily reliant on high‑volume digital marketing

Dashdot’s co-founder Goose McGrath penned an open letter detailing the grim reality facing Australia’s real estate industry and the consumer economy more generally.

Macroeconomic shock (Feb–May 2026):

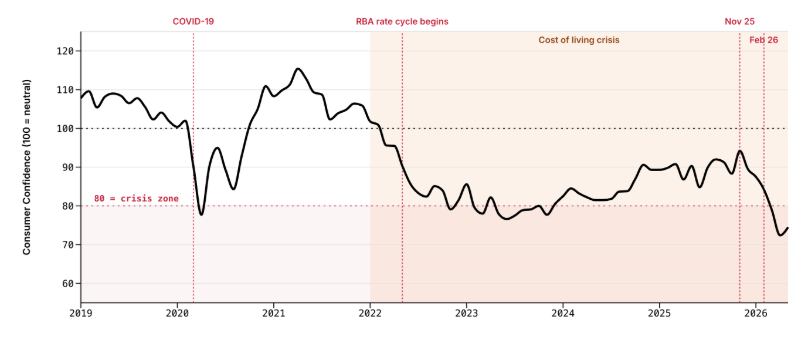

McGrath notes that “coming into 2026, Australian households were already deep in a sustained cost-of-living crisis that had been building since 2022, and had not eased”.

“Inflation continued to push prices, and the cost of living, up throughout 2025”.

“The Federal Energy Bill Relief Fund, which had been softening household power bills for two years, ended on 31 December 2025”.

“Australia had been in a per capita recession for most of the prior two years, with real living standards going backwards”…

“By any measure, Australians were already in crisis mode”.

“Then, from early February 2026, the conditions began to worsen”…

McGrath notes that a severe deterioration in Australia’s economic environment crushed consumer confidence — the key driver of Dashdot’s business model.

Key pressures cited include the following:

- APRA’s first-ever cap on high debt‑to‑income lending

- RBA three rate hikes (to 4.35%)

- A global oil shock after conflict in Iran, pushing petrol above $2.50/L

- Consumer Confidence collapsing to the lowest sustained level in 50+ years

- Mortgage stress rising to 35–40% worse than peak COVID

- Roy Morgan’s real unemployment at 10.1%; underutilisation at 20.9%

The above factors created a market where everyday Australians were in “crisis mode”, unwilling or unable to invest.

Policy shock: Federal Budget 2026:

McGrath notes that the May federal budget delivered the biggest property tax changes in nearly 30 years, triggering investor paralysis, namely:

- The CGT discount was removed for future investors (replaced with indexation plus a 30% minimum tax)

- Negative gearing was limited to new builds only

Banks responded within days, with Westpac, then Macquarie, then the big four removing negative gearing benefits from lending calculators

As a result, investor borrowing capacity fell 20–33% overnight, freezing investor activity.

Combined with internal fragilities, these macroeconomic forces made Dashdot’s business unviable within weeks.

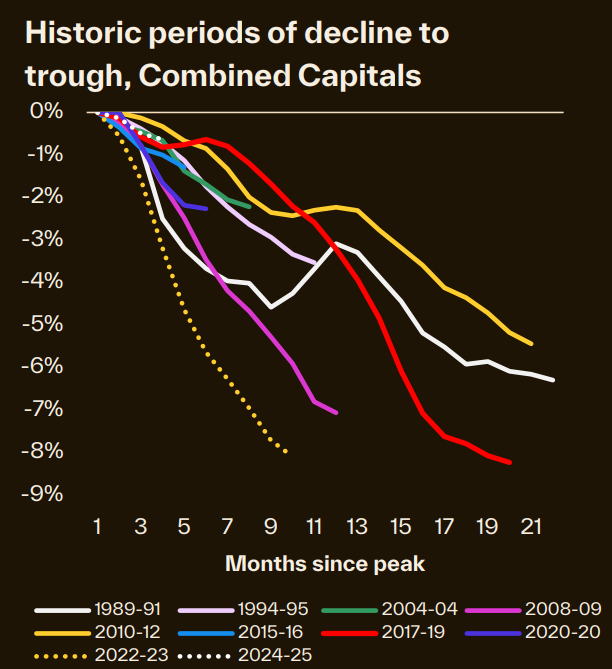

Lessons for the broader housing market:

The above macroeconomic forces are why I believe that Australia’s housing market faces its biggest price correction in 40 years.

Source: Cotality

The combination of overvaluation, rising interest rates, worsening sentiment, and the federal budget’s changes to negative gearing and capital gains taxes has combined to create the ‘perfect storm’ for the housing market.