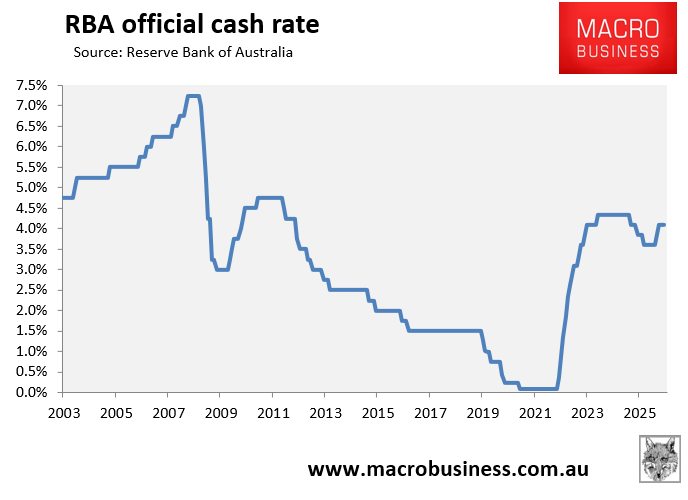

Last week’s 25 bp hike in the official cash rate by the Reserve Bank of Australia (RBA) – the third consecutive increase – may have been the ‘straw that broke the camel’s back’.

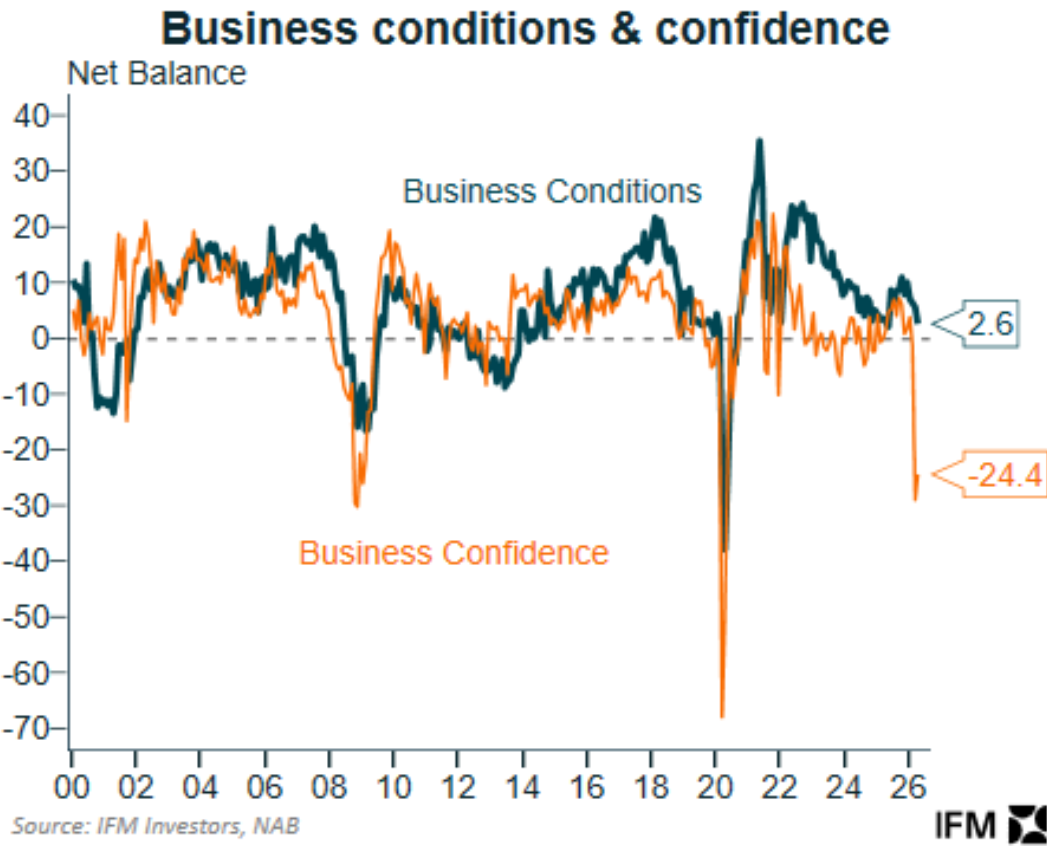

As illustrated below by Alex Joiner from IFM Investors, NAB’s business survey showed that business confidence remains in deeply pessimistic territory, while conditions (which track GDP growth more tightly) have continued to soften:

“The risk for the RBA, is that the deterioration we are observing in the leading indicator data leads to a greater than expected slowdown in the hard data”, noted Joiner via Twitter (X).

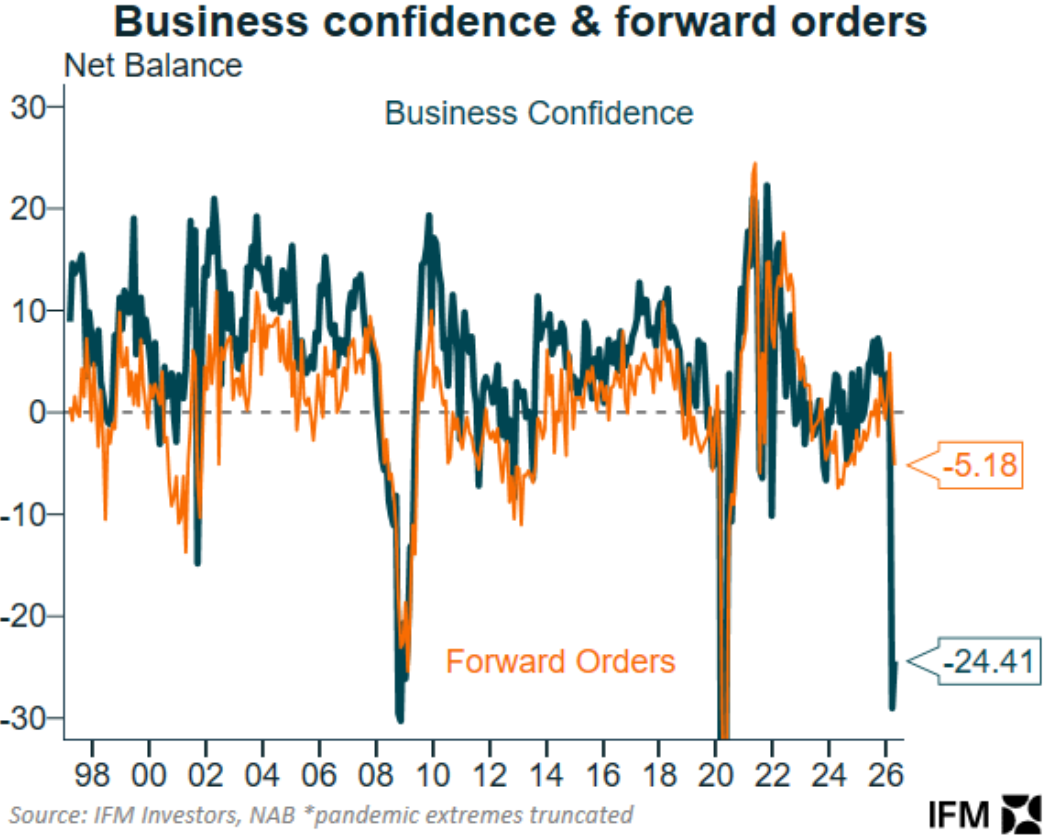

Joiner added that “the fall in business confidence has started to weigh more materially on forward orders”:

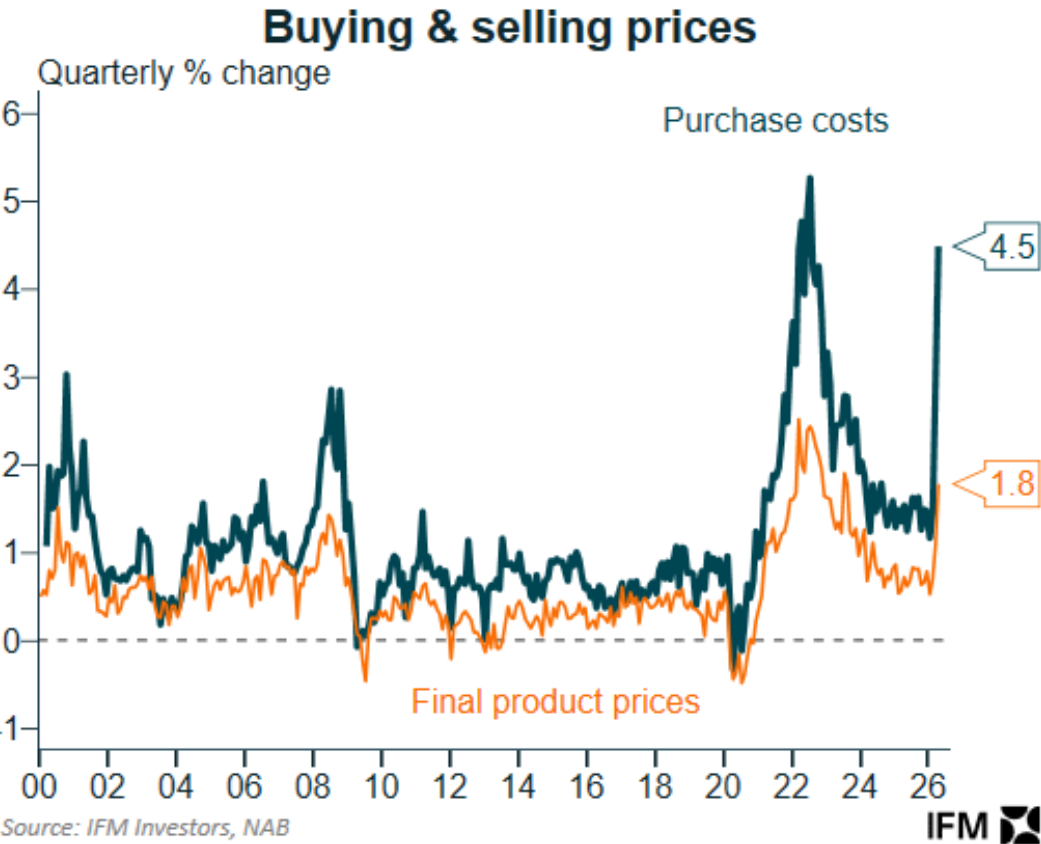

Meanwhile, as flagged in last week’s media conference by RBA governor Michele Bullock, second-round inflation impacts from rising fuel prices are incoming, with businesses set to pass on costs to consumers:

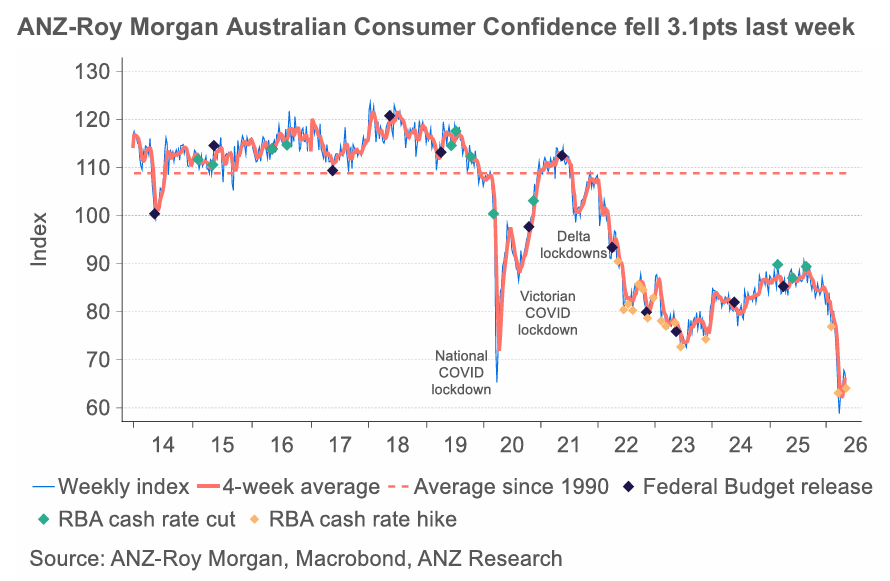

The data is equally grim on the consumer side, with the latest weekly ANZ-Roy Morgan consumer confidence survey recording a heavy 3.1-point fall last week after the RBA hikes rates, with the overall confidence index recording its fourth weakest print in around 50 years:

“At 64.1pts, confidence is at its fourth-lowest level since the series began in 1973. All subindices declined, led by a sharp fall in household confidence in personal finances”, ANZ economist Sophia Angala reported.

My expectations remain that the RBA will repeat the 2007 to 2008 Global Financial Crisis (GFC) experience, whereby it hiked rates aggressively (by 100 basis points) into the US subprime mortgage crisis, only to then cut rates hard from September 2008 when the full-blown GFC landed.

After another one or two rate hikes this year, I can see the RBA cutting rates aggressively next year as a recession takes hold.