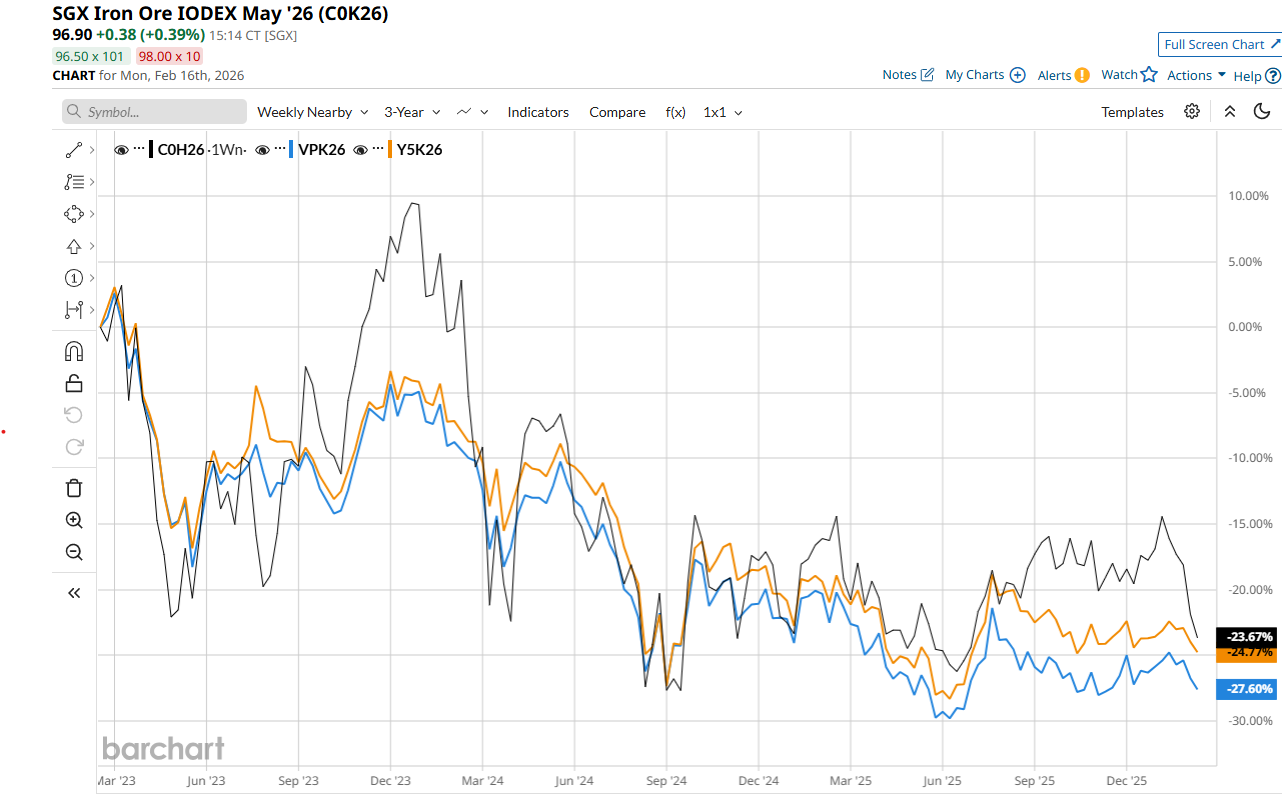

The ferrous jaws are all but closed after a Friday flush.

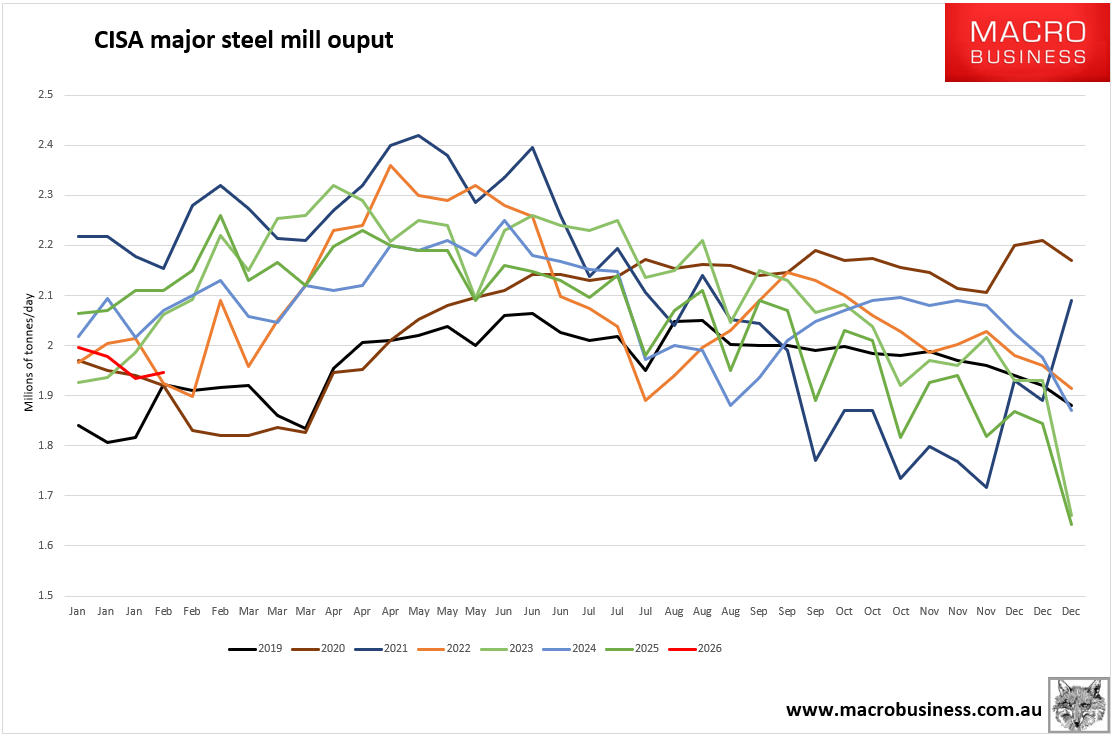

CISA early February data was out and was not good. We are well below 2025 output here, though the later CNY is playing a role.

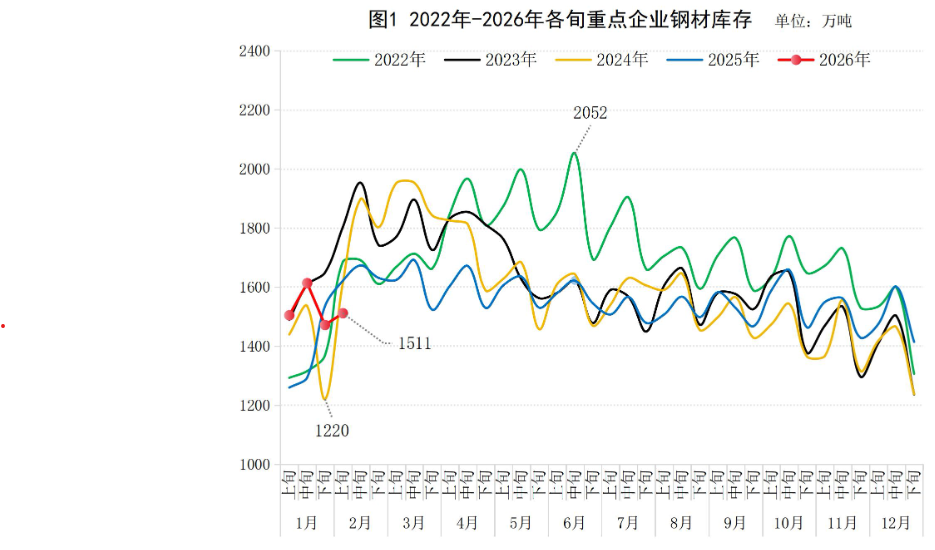

Steel inventories climbed 2.7%.

As you can see, mills are about to pile it up over the Chinese New Year. But the stockpile only needs to build 2mt to meet last year’s level. It’s hardly a restock at all.

Meanwhile, get this indya.

Kpler analyst Alexis Ellender said he had tracked just 1.18 million tonnes of Jimblebar Fines leaving Australia in January, which was down from 5.82 million tonnes in January 2025.

Ellender said there were 70 ships parked off the Chinese coast waiting to discharge their iron ore, which was higher than at the same time last year.

“After a period of sustained growth, we believe iron ore port stockpiles in China are close to capacity. This has slowed cargo discharge,” he said.

Seasonally, port inventories typically top about now. But with so much excess iron ore piling up everywhere and backlogging at Chinese ports, the port inventory peak might hold.

If there is no more room for China to expand its iron ore great pyramids, then the marginal absorber of excess supply is about to exit the market, and the price will crash.

On top of this, BHP’s Jimblebar debacle has it shipping roughly 56mt less iron ore annualised, and the spot iron ore price is still falling fast.

CMRG should open the Jimblebar valve, and the iron ore spot price will crash even harder.

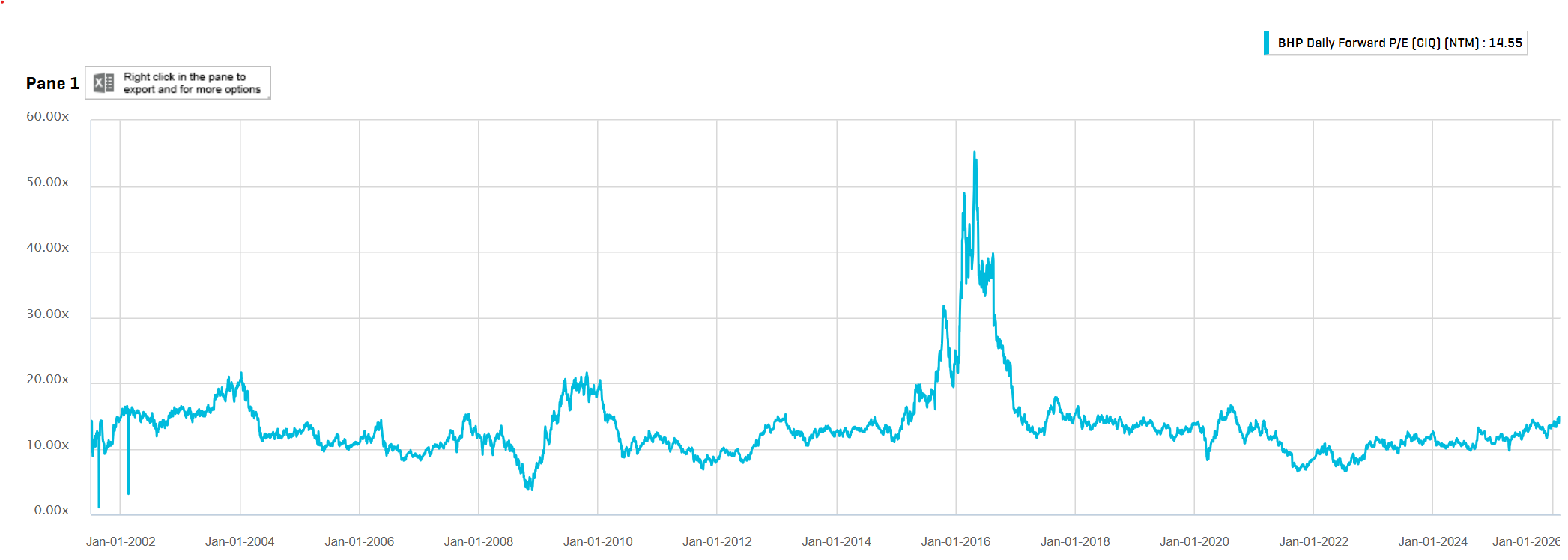

It is hilarious that while this is happening, the BHP share price has rallied to 15XNTM, its highest in four years, even as 60% of its profits are on fire in a dumpster.

Well, guess what? NTM is about to rocket because profits are going to crater.

A drop of iron ore to $85 would rip roughly $5bn out of BHP EBTIDA, and there goes your dividend.

The strong AUD makes it even worse.

And I haven’t even mentioned RIO’s Simandou, which pumps harder and harder non-stop for the next three years.

For those with a memory, it was RIO that crashed iron ore in 2015 with a volume-over-value strategy. It has done it again, this time accidentally! With no bailout mechanism because it is partnered with China.

The big miners have been the darlings of the American madman trade, which is mad in itself.

Now they are on a cliff edge, below which there is nothing but falling profits and cut dividends for as far as the eye can see.

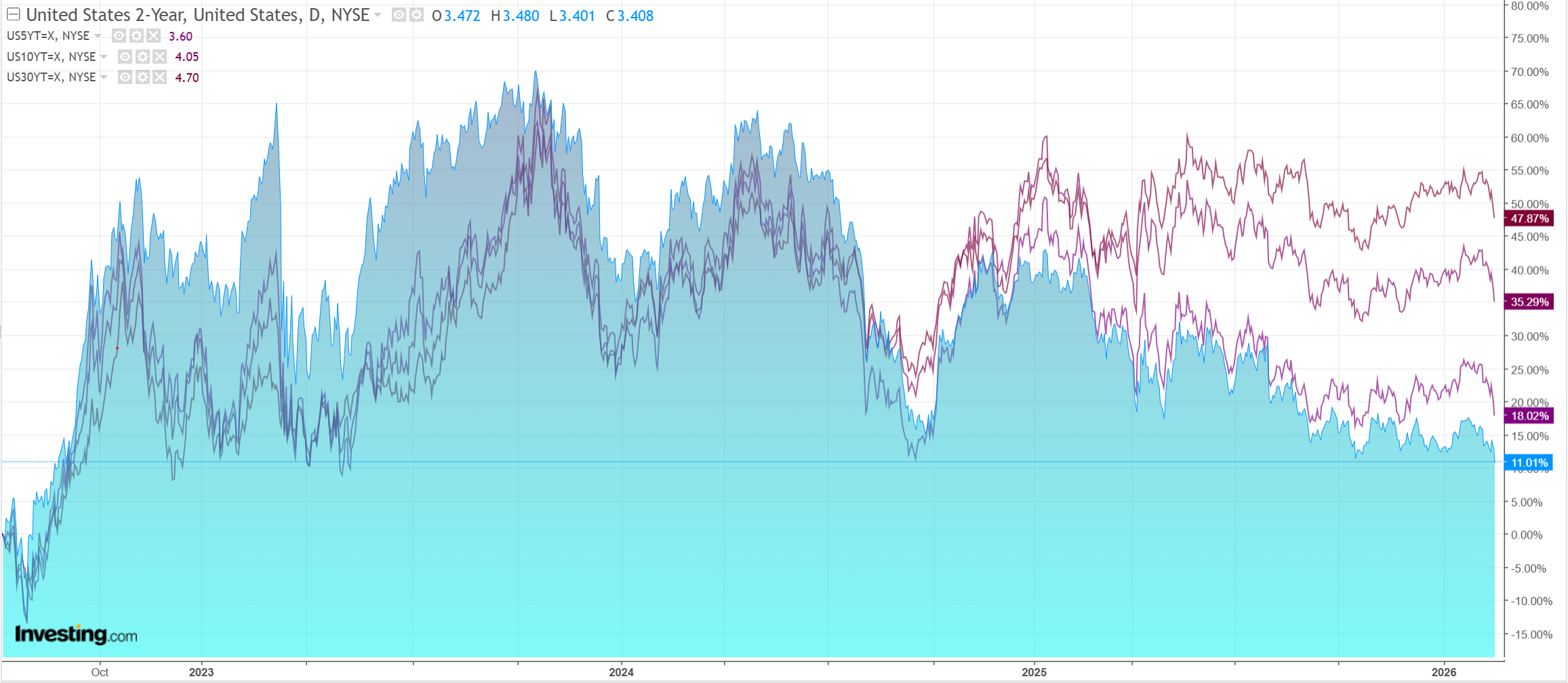

Turning to the AUD, we are about to stress test its relationship with the red dirt.

On Friday night, DXY held up despite better-than-expected inflation.

However, AUD did not hold up. It has run hard, and maybe it’s just a bit of fatigue. But if iron ore falls into the $80s and starts to drag on Aussie yields, let alone to a real shakeout price, this little AUD bull is going to meet a large red bear.

Gold ran higher on US rate cut hopes, but oil sank despite a second carrier headed to bomb, bomb, bomb…bomb, bomb Iran.

AI metals look a little shaky here. Imagine if copper were dumped with iron ore.

The diversified miners would be slaughtered. All parabolas collapse, and this one was bonkers from the outset.

EM stocks won’t like it, either.

Junk just doesn’t care. It’s all rotational. Nothing macro.

Treasury yields rallied hard on cool US inflation.

Stocks tried but couldn’t.

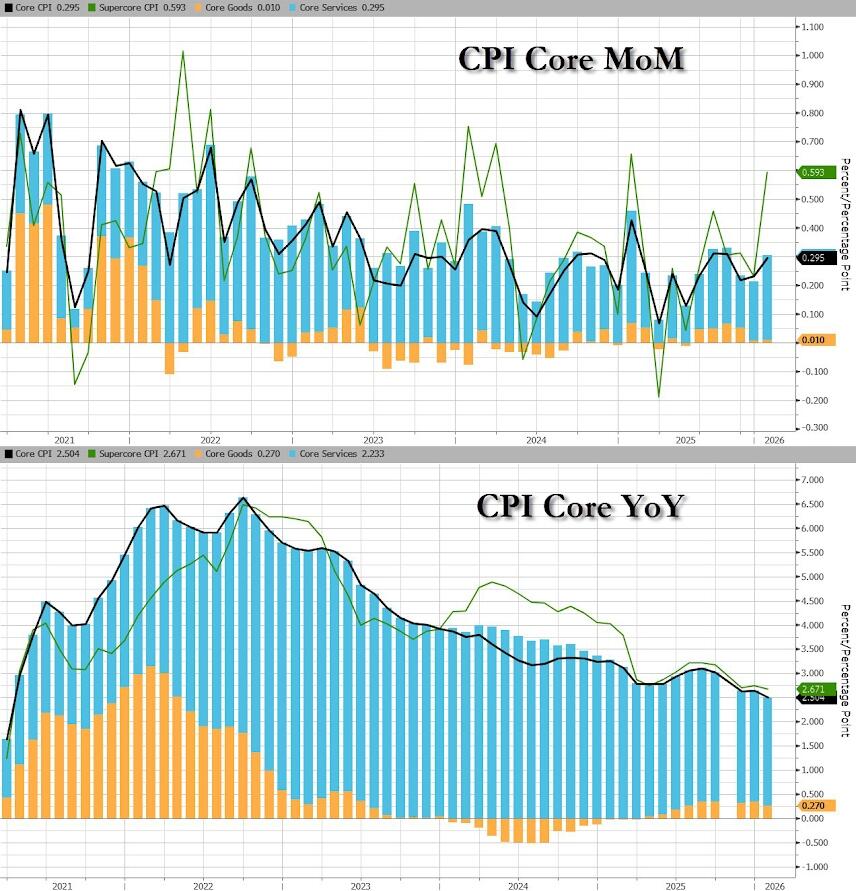

The US headline was soft at 0.2%, but core inflation was bang on 0.3%. Both sank Yoy.

There isn’t any tariff inflation. Services have firmed recently and will need to resume disinflation before those juicy low-inflation months in 2025 drop out of the series.

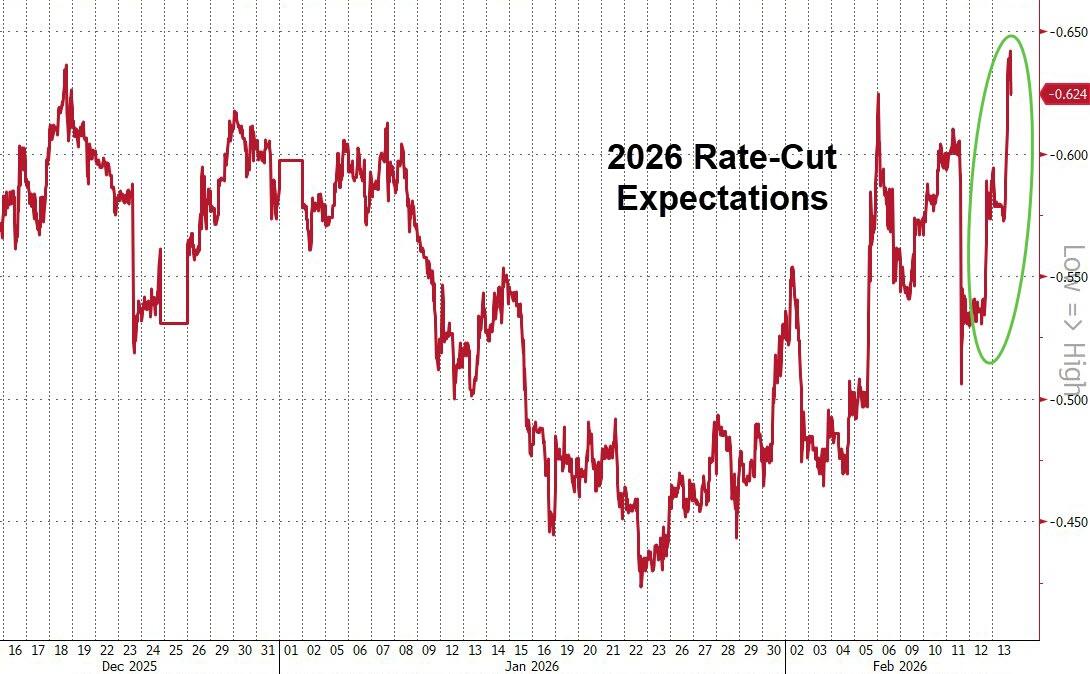

But overall, decent enough to lift hopes for a rate cut to a 2026 high.

This is put ongoing pressure on DXY, but I maintain that we are past ‘peak debasement’ as Trump recalibrates for the midterms.

Once he’s done with Iran, which seems likely to be some worthless new bombing campaign with a declaration of “mission accomplished” at the end, the madness of 2026 will be over, to save the polls.

With the rising possibility that iron ore outright crashes dead ahead, AUD may be on the verge of reverting to its former cyclical glory.