I am an avid follower of leading Sydney auctioneer Tom Panos. I always watch his Saturday auction market report on YouTube for insight into the market’s pulse and developments in the real estate industry.

In this weekend’s update, Panos took direct aim at the Albanese government’s rumoured changes to the capital gains tax (CGT) discount, which could reduce it from its current 50% to 25%.

Such a change in the CGT discount would make investment in property significantly less attractive by reducing after-tax returns.

Panos claimed that “the fabric of real estate in Australia is on the verge of being changed forever” and that any changes to the CGT discount would have “unintended consequences”, in particular for “tenants who are the most vulnerable cohort people of Australia , who will get impacted because rents will go up”.

Panos argues that rents will necessarily increase because “there’s going to be less rental properties and basic demand and supply says rents are going to be pushed up”.

“Really, we’re going to end up seeing rents rise. No question about it. Because if investor supply sort of vanishes, rents are going to rise”, Panos argued.

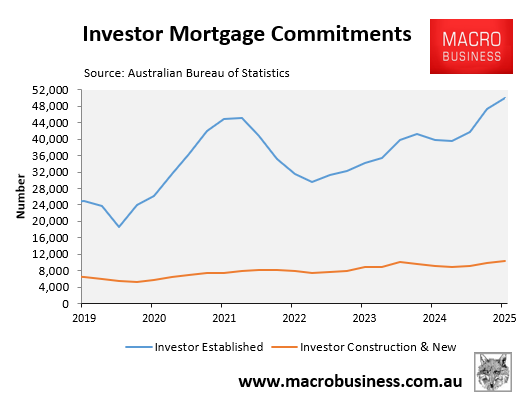

Last week’s housing finance data from the Australian Bureau of Statistics (ABS) showed that property investors overwhelmingly purchase established dwellings over new builds:

In 2025, 82% of loans to investors were for established dwellings, according to the ABS.

Therefore, property investors are pumping up demand far more than they are contributing to new housing supply.

The notion that renters will suffer if fewer investors enter the market or sell properties is fundamentally flawed. The property does not disappear.

Instead, the property will either be purchased by another investor or by an owner-occupier (including a first home buyer).

As a result, the balance between rental supply and demand will not change. There will be fewer investors and more owner-occupiers. There will be fewer homes available for rent, but fewer people will need to rent.

If Panos’ argument that an investor exodus would drive up rents was true, then Melbourne tenants should have experienced the largest rent rises in the nation.

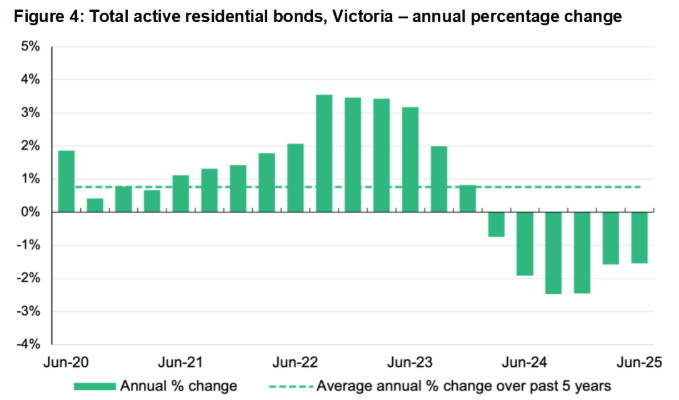

In 2024, the Victorian government implemented tax increases and new levies that considerably increased holding costs for investors. These included reduced land tax thresholds, higher vacant land taxes, and new short-stay levies.

As a result of the reforms, more property investors in Victoria are now paying land tax, and those who have previously paid are paying more.

With the holding costs for investment properties having risen dramatically, lowering net yields, a substantial number of investors have abandoned the market, as demonstrated by the reduction in the number of rental bonds on issue:

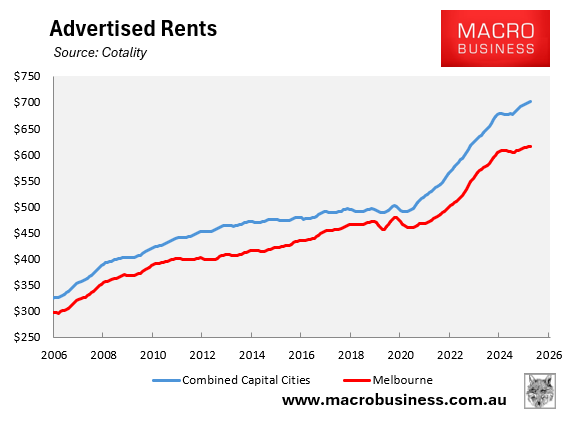

However, the reduction of investors has not driven Melbourne rents higher or reduced affordability.

According to Cotality, Melbourne advertised rents increased by 36% in the five years to January 2026, a significantly smaller increase than the 43% rise observed across the combined capital cities.

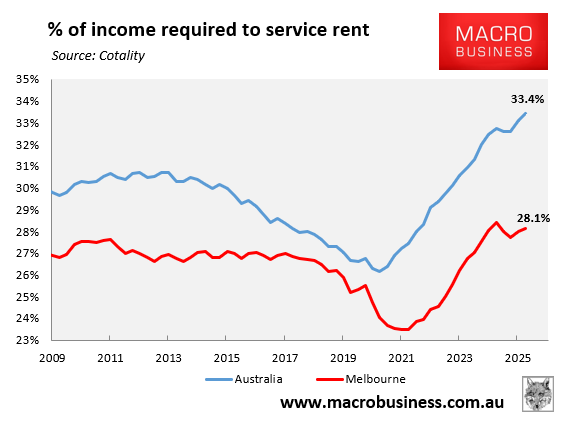

As of the September quarter of 2025, the percentage of income required to rent the median home in Melbourne was 28.1%, which was significantly lower than the national average of 33.4%.

As illustrated above, Melbourne’s rental affordability has actually improved over the past year, whereas it has worsened across the nation as a whole.

Therefore, the data from Cotality shows that Melbourne’s rental affordability is significantly more favourable than the national average, despite the flight of property investors caused by the government’s tax reforms.

Melbourne demonstrates why changes to the CGT discount are unlikely to harm the nation’s rental markets.

While there will undoubtedly be fewer investors in the market, the loss of rental availability will be countered by an increase in first home buyers and a decrease in renters seeking housing.

There is no reason for renters to be concerned about changes to the CGT discount. On the other hand, first home buyers will face less competition from investors, which is likely to lead to an improvement in homeownership rates.

All that being said, changes to the CGT discount will have a minor impact on the housing market overall, and far greater benefits could be gained by running a significantly smaller and better targeted immigration system.

On this point, I wholeheartedly agree with Tom Panos:

“They should be looking at migration and making sure it’s aligned to the amount of properties that are being built because the speed of migration is higher than the speed of properties being built. That’s the first thing”.

“And if you’re going to do migration, start bringing in proper tradespeople so we can reduce labour costs”.

The reality is that the rental crisis in Australia will remain as long as the federal government keeps importing demand faster than new housing can be supplied.

Changes to the CGT discount won’t change Australia’s structural housing imbalance. Only a smaller and better targeted migration system can do that.